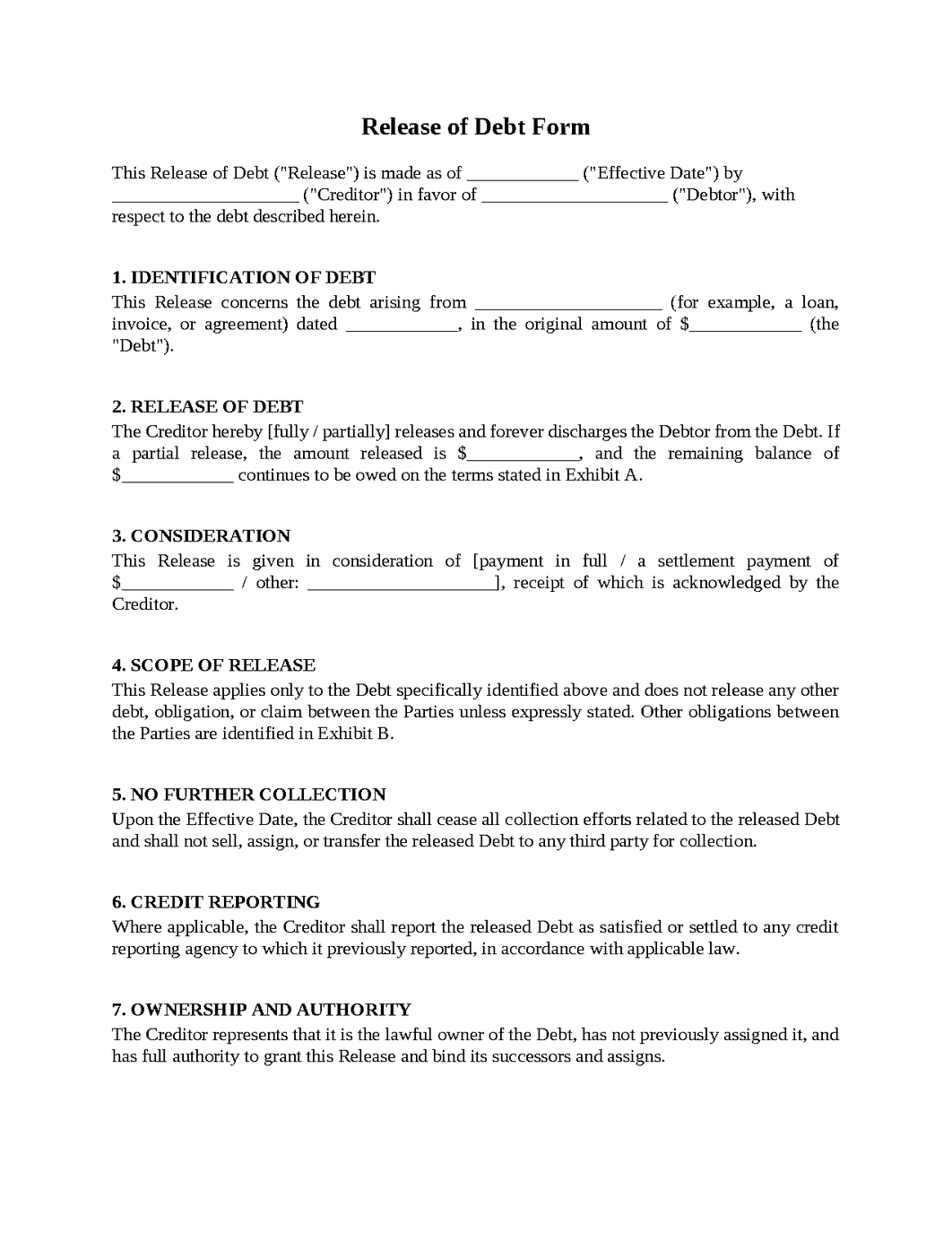

Release of Debt Form

A Release of Debt Form is a legal document used to formally acknowledge that a debt, loan, financial obligation, or payment responsibility has been satisfied, forgiven, settled, discharged, or otherwise released. These forms are commonly used in private loans, business transactions, settlement agreements, family lending arrangements, commercial obligations, and creditor-debtor relationships. A Release of Debt Form helps provide written evidence that the debtor no longer owes the specified obligation and that the creditor waives future collection rights related to the released debt. Because financial obligations often involve significant amounts of money and long-term records, disputes can arise when debt satisfaction is not documented clearly. A well-prepared Release of Debt Form helps protect both parties and reduce future misunderstandings.

The Debtor Believes the Debt Was Fully Forgiven

A business owner experiences financial difficulties and negotiates with a creditor to resolve an outstanding obligation.

After several discussions, the debtor makes a substantial payment that is intended to settle the matter. The debtor believes the payment fully satisfies the debt and ends all future obligations. The creditor believes the payment resolves only a portion of the balance and expects additional payments in the future.

Months later, collection efforts resume and the debtor is surprised to learn that the creditor still considers money to be owed.

The disagreement develops because the settlement discussions were never documented clearly.

Both parties recall the negotiations differently and rely on conflicting interpretations of what was agreed.

To help avoid this problem, a Release of Debt Form should clearly identify the debt being released, specify whether the release is partial or complete, and confirm that no additional amounts remain due after the release becomes effective.

Collection Efforts Continue After Payment

An individual repays a private loan according to a negotiated settlement arrangement.

The creditor accepts payment and considers the matter resolved. Several years later, however, records maintained by a collection agency still show an outstanding balance associated with the obligation.

The debtor begins receiving collection notices regarding a debt that was already paid and released. The creditor no longer has detailed records readily available and must reconstruct events that occurred years earlier.

What should have been a closed matter becomes a frustrating dispute because proof of the release is difficult to locate.

The situation creates unnecessary stress and administrative expense for everyone involved.

To reduce these risks, a Release of Debt Form should be executed promptly after satisfaction of the obligation and retained by both parties for future reference. Clear documentation helps prevent mistaken collection activity.

Multiple Obligations Exist Between the Same Parties

A business maintains several financial relationships with a vendor, including loans, payment plans, and outstanding invoices.

When one obligation is resolved, the parties execute documentation acknowledging payment. Later, questions arise regarding whether the release applies only to the specific debt that was satisfied or to all obligations between the parties.

The debtor believes the release was broad and comprehensive. The creditor believes it applied only to one particular obligation.

The disagreement becomes complicated because multiple transactions occurred over an extended period of time.

Neither side intended confusion, but the release language lacks sufficient specificity.

To help prevent these issues, a Release of Debt Form should clearly identify the exact debt being released and specify whether the release applies to one obligation or multiple obligations. Detailed descriptions help eliminate uncertainty.

A Business Is Sold and Old Debts Resurface

A company is sold to new owners after years of operation.

During the transaction, the parties review financial records and believe certain historical debts were settled previously. After the sale closes, a former creditor claims that an outstanding obligation remains unpaid.

The new owners request documentation showing that the debt was released. The prior owners insist the matter was resolved years ago but struggle to locate supporting records.

The dispute creates uncertainty regarding who is responsible for the alleged obligation and whether the debt still exists.

What should have been a completed transaction becomes a problem because documentation was not preserved properly.

To help avoid these problems, a Release of Debt Form should be maintained with financial records and transaction documents so that evidence of debt satisfaction remains available if questions arise later.

Family Members Disagree About a Personal Loan

A parent lends money to an adult child to help with a home purchase and later decides to forgive the remaining balance.

The family views the arrangement as informal and based on trust. The parent communicates that repayment is no longer necessary, and everyone assumes the matter is resolved.

Years later, estate administration begins after the parent's death. Other family members question whether the loan was truly forgiven and whether the unpaid balance should be treated as part of the estate.

Because no written release exists, family members disagree regarding the parent's intentions.

A situation that could have been documented easily becomes a source of conflict among relatives.

To reduce these risks, a Release of Debt Form should be used whenever a debt is forgiven, even in family situations. Written confirmation helps ensure that future generations understand the parties' intentions.

Release of Debt Forms play an important role in documenting the satisfaction, settlement, or forgiveness of financial obligations. However, issues involving settlement terms, continued collection efforts, multiple obligations, business transactions, and family loans can become significant sources of conflict when debt releases are not documented clearly. A carefully prepared Release of Debt Form provides a structured framework for confirming that obligations have been resolved and protecting both debtors and creditors. When prepared thoughtfully, it can help reduce misunderstandings, prevent future disputes, preserve important records, and provide certainty that a financial obligation has truly come to an end.

Get started with Upsign today!

Easily send, sign and track your documents